Mortgage - Interest Rates and Points - understanding

What are (discount) points and lender credits and how do they work?

Generally, points and lender credits let you make tradeoffs in how you pay for your mortgage and closing costs. Points, also known as discount points, lower your interest rate in exchange paying for an upfront fee. Lender credits lower your closing costs in exchange for accepting a higher interest rate.

These terms can sometimes be used to mean other things. “Points” is a term that mortgage lenders have used for many years. Some lenders may use the word “points” to refer to any upfront fee that is calculated as a percentage of your loan amount, whether or not you receive a lower interest rate. Some lenders may also offer lender credits that are unconnected to the interest rate you pay – for example, as a temporary offer, or to compensate for a problem.

The information below refers to points and lender credits that are connected to your interest rate. If you’re considering paying points or receiving lender credits, always ask lenders to clarify what the impact on your interest rate will be.

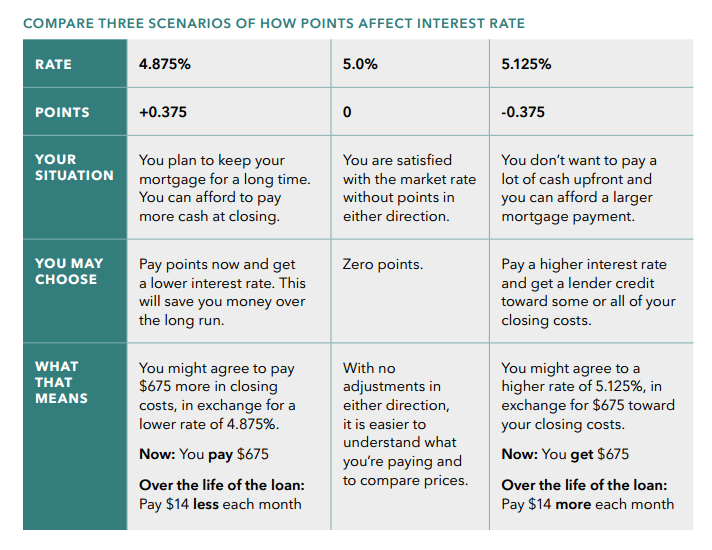

See an example:

The chart below shows an example of the tradeoffs you can make with points and credits. In the example, you borrow $180,000 and qualify for a 30-year fixed-rate loan at an interest rate of 5.0% with zero points. In the first column, you choose to pay points to reduce your rate. In third column, you choose to receive lender credits to reduce your closing costs. In the middle column, you do neither.

Tip: If you don’t know how long you’ll stay in the home or when you’ll want to refinance and you have enough cash for closing and savings, you might not want to pay points to reduce your interest rate, or take a higher interest rate to receive credits. If you are unsure, ask a loan officer to show you two different options (with and without points or credits) and to calculate the total costs over a few different possible timeframes. Choose the shortest amount of time, the longest amount of time, and the most likely amount of time you can see yourself keeping the loan. You can also review your options with a HUD-certified housing counselor.

When comparing offers from different lenders, ask for the same amount of points or credits from each lender.

Source: CFPB